It was July 26, 2007 when Manitoba Hydro dropped the bombshell on the Public Utilities Board.

The drought of 2003-2004 had traumatized Hydro. It knocked the stuffing out of Hydro's finances-more damage in a single year than anyone ever imagined. The utility ramped up computer simulations to show the board what the cost would be of a multi-year drought like, say, the five that have happened since 1929.

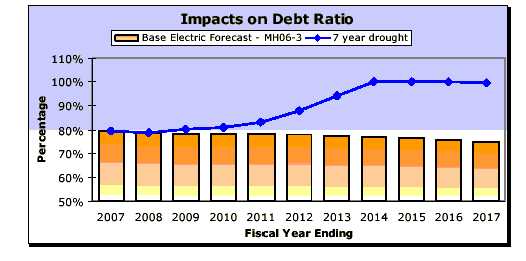

It wasn't a pretty picture.

A five year drought would cost Manitoba Hydro $2.7 billion.

A seven-year drought would cost $3.5 billion.

The numbers may be gi-normous, but that's not what made the PUB blanche. It was the graphs.

A five year drought (starting in 2008 for demonstration purposes) would increase the debt-to-equity position of Hydro to 95-5. That's like making Manitoba Hydro a penny stock.

Ask the Aspers what that did for Canwest Global shares, if you can catch them between meetings with their bankruptcy lawyers.

Oh, and a seven year drought would wipe out all of Hydro's equity

Given the high stakes, the PUB has become obsessed with drought. At first glance, that might seem unwarranted.

A five-year drought is expected once in 50 years, and the last one was only 18 years ago, 1987-91.

A seven year drought is one in 100 year phenomenon and the last was 1936-42.

But…a drought like the one that ravaged Hydro in 2003-2004 happens once ever 15 years---and another one is expected in the coming decade.

The PUB is worried that Hydro's management is not taking enough precautions. A special concern is Hydro's $18 billion plan for new dams to supply American customers.

Here's how the PUB raised the issue in a recent order:

"The 2003-04 drought demonstrated that MH's generally "aggressive" approach to export energy marketing, while conducive to higher profits in median or above flow scenarios, carries the risk of increased losses during drought or low flow years. MH has acknowledged this risk, but believes its present strategy (that is, depending on median water flows) provides greater longer-term financial returns. The Board is not so certain and would prefer an independent assessment be conducted and filed."

The PUB cited one example of how this "aggressive" approach to selling power to the U.S. backfired on Manitoba customers. Hydro sold power it didn't have, then had to be bailed out by a rise in rates.

"Some of MH's exports involve three to four month advance sales of firm energy, without the certainty that the firm energy sold will be available (i.e., precipitation may not replenish water resources). Such practices lead to reasonable results in the absence of poor water conditions, but significant cost consequences when water flows fall and imports have to be purchased to fulfill contract obligations.

This situation occurred in the summer of 2006/07 and, in the Board's view, contributed to MH's request for a 2.25% interim rate increase (granted initially as an interim increase and finalized by Order 90/08)."

There's a pattern of mismanaging water resources, according to the PUB's examples. In the '03-'04 drought, Manitoba Hydro exacerbated the losses by selling off power at cheap prices, then buying it back at a higher cost to meet obligations to American customers.

"MH cannot prevent droughts from occurring, but, arguably, could do more than was done in 2003/04 to mitigate the consequences of a multi-year drought. In 2003/04, energy from water held in reserves was sold at low prices (off-peak pricing) to boost that year's annual income, only for the energy to be required to be "bought back" from the MISO market to meet MH's export commitments, and then at much higher prices than what the energy was sold for."

And the PUB warns that power shortages (the kind that lead to power brownouts) are a possibility if Hydro's dam building suffers any unpredicted delays.

"10.4 New Generation and Transmission

MH is proceeding with the Wuskwatim Generating Station with a targeted in-service date of 2012/13. An Agreement has been reached with WPLP for purchase of all output, estimated to be 1,515 GW.h on average. This arrangement is expected to provide a 1,220 GW.h increase in MH's dependable power (4%).

Bipole III is slated to be in-service in 2017/18, and is expected to add 442 GW.h/yr to MH's dependable generation, this by reducing transmission losses on the HVDC system. The loss reduction could be 1,000 GW.h under average flow conditions, based on the existing Upper Nelson generation plant.

MH's 2007/08 Power Resource Plan indicates that by 2017/18 total generation plant output under a dependable flow scenario will be 28,845 GW.h, equal to base domestic load. At that point, and until Conawapa and Keeyask G.S. are constructed, exports would have be supplied from domestic load reductions, through DSM (demand side management) and by imports or MH natural gas generation."

And….

"In the absence of Keeyask, MH's dependable domestically generated energy of, then forecast to be, about 30,000 GW.h would just cover forecast 2022/23 base domestic load. In such a case meeting the new export commitments would require further domestic load reductions through DSM savings and additional imports or MH natural gas generation.

If either space heating conversions from natural gas to electricity occurred or new large industry or large industry expansion drew power, the situation would be more problematic."

Bankruptcy? Impossible.

Brownouts and blackouts? Impossible.

Oh yeah?

-30-

The drought of 2003-2004 had traumatized Hydro. It knocked the stuffing out of Hydro's finances-more damage in a single year than anyone ever imagined. The utility ramped up computer simulations to show the board what the cost would be of a multi-year drought like, say, the five that have happened since 1929.

It wasn't a pretty picture.

A five year drought would cost Manitoba Hydro $2.7 billion.

A seven-year drought would cost $3.5 billion.

The numbers may be gi-normous, but that's not what made the PUB blanche. It was the graphs.

A five year drought (starting in 2008 for demonstration purposes) would increase the debt-to-equity position of Hydro to 95-5. That's like making Manitoba Hydro a penny stock.

Ask the Aspers what that did for Canwest Global shares, if you can catch them between meetings with their bankruptcy lawyers.

Oh, and a seven year drought would wipe out all of Hydro's equity

Given the high stakes, the PUB has become obsessed with drought. At first glance, that might seem unwarranted.

A five-year drought is expected once in 50 years, and the last one was only 18 years ago, 1987-91.

A seven year drought is one in 100 year phenomenon and the last was 1936-42.

But…a drought like the one that ravaged Hydro in 2003-2004 happens once ever 15 years---and another one is expected in the coming decade.

The PUB is worried that Hydro's management is not taking enough precautions. A special concern is Hydro's $18 billion plan for new dams to supply American customers.

Here's how the PUB raised the issue in a recent order:

"The 2003-04 drought demonstrated that MH's generally "aggressive" approach to export energy marketing, while conducive to higher profits in median or above flow scenarios, carries the risk of increased losses during drought or low flow years. MH has acknowledged this risk, but believes its present strategy (that is, depending on median water flows) provides greater longer-term financial returns. The Board is not so certain and would prefer an independent assessment be conducted and filed."

The PUB cited one example of how this "aggressive" approach to selling power to the U.S. backfired on Manitoba customers. Hydro sold power it didn't have, then had to be bailed out by a rise in rates.

"Some of MH's exports involve three to four month advance sales of firm energy, without the certainty that the firm energy sold will be available (i.e., precipitation may not replenish water resources). Such practices lead to reasonable results in the absence of poor water conditions, but significant cost consequences when water flows fall and imports have to be purchased to fulfill contract obligations.

This situation occurred in the summer of 2006/07 and, in the Board's view, contributed to MH's request for a 2.25% interim rate increase (granted initially as an interim increase and finalized by Order 90/08)."

There's a pattern of mismanaging water resources, according to the PUB's examples. In the '03-'04 drought, Manitoba Hydro exacerbated the losses by selling off power at cheap prices, then buying it back at a higher cost to meet obligations to American customers.

"MH cannot prevent droughts from occurring, but, arguably, could do more than was done in 2003/04 to mitigate the consequences of a multi-year drought. In 2003/04, energy from water held in reserves was sold at low prices (off-peak pricing) to boost that year's annual income, only for the energy to be required to be "bought back" from the MISO market to meet MH's export commitments, and then at much higher prices than what the energy was sold for."

And the PUB warns that power shortages (the kind that lead to power brownouts) are a possibility if Hydro's dam building suffers any unpredicted delays.

"10.4 New Generation and Transmission

MH is proceeding with the Wuskwatim Generating Station with a targeted in-service date of 2012/13. An Agreement has been reached with WPLP for purchase of all output, estimated to be 1,515 GW.h on average. This arrangement is expected to provide a 1,220 GW.h increase in MH's dependable power (4%).

Bipole III is slated to be in-service in 2017/18, and is expected to add 442 GW.h/yr to MH's dependable generation, this by reducing transmission losses on the HVDC system. The loss reduction could be 1,000 GW.h under average flow conditions, based on the existing Upper Nelson generation plant.

MH's 2007/08 Power Resource Plan indicates that by 2017/18 total generation plant output under a dependable flow scenario will be 28,845 GW.h, equal to base domestic load. At that point, and until Conawapa and Keeyask G.S. are constructed, exports would have be supplied from domestic load reductions, through DSM (demand side management) and by imports or MH natural gas generation."

And….

"In the absence of Keeyask, MH's dependable domestically generated energy of, then forecast to be, about 30,000 GW.h would just cover forecast 2022/23 base domestic load. In such a case meeting the new export commitments would require further domestic load reductions through DSM savings and additional imports or MH natural gas generation.

If either space heating conversions from natural gas to electricity occurred or new large industry or large industry expansion drew power, the situation would be more problematic."

Bankruptcy? Impossible.

Brownouts and blackouts? Impossible.

Oh yeah?

-30-